Case study · Moneyfellows

Designing for credit risk

Leading design on credit assessment — an ML model built with the data science team, and the experience that made it work.

−12%

default rates

56M EGP

decrease in exposure

+10%

retention lift

Context

Moneyfellows digitizes money circles — the rotating savings groups (ROSCAs) that much of the region already runs on trust. Digitizing trust means underwriting it: when a member receives their payout early in the circle, the company is carrying real credit risk. Getting that assessment right is not a feature; it's the business.

The project

The credit assessment work was driven by a Central Bank of Egypt licensing requirement, which put it at the center of the company's regulatory and business agenda at once. I led design on it, working directly with the data science team implementing the ML risk model, and owning the side of the system users actually touch: how credit limits are communicated, earned, and understood.

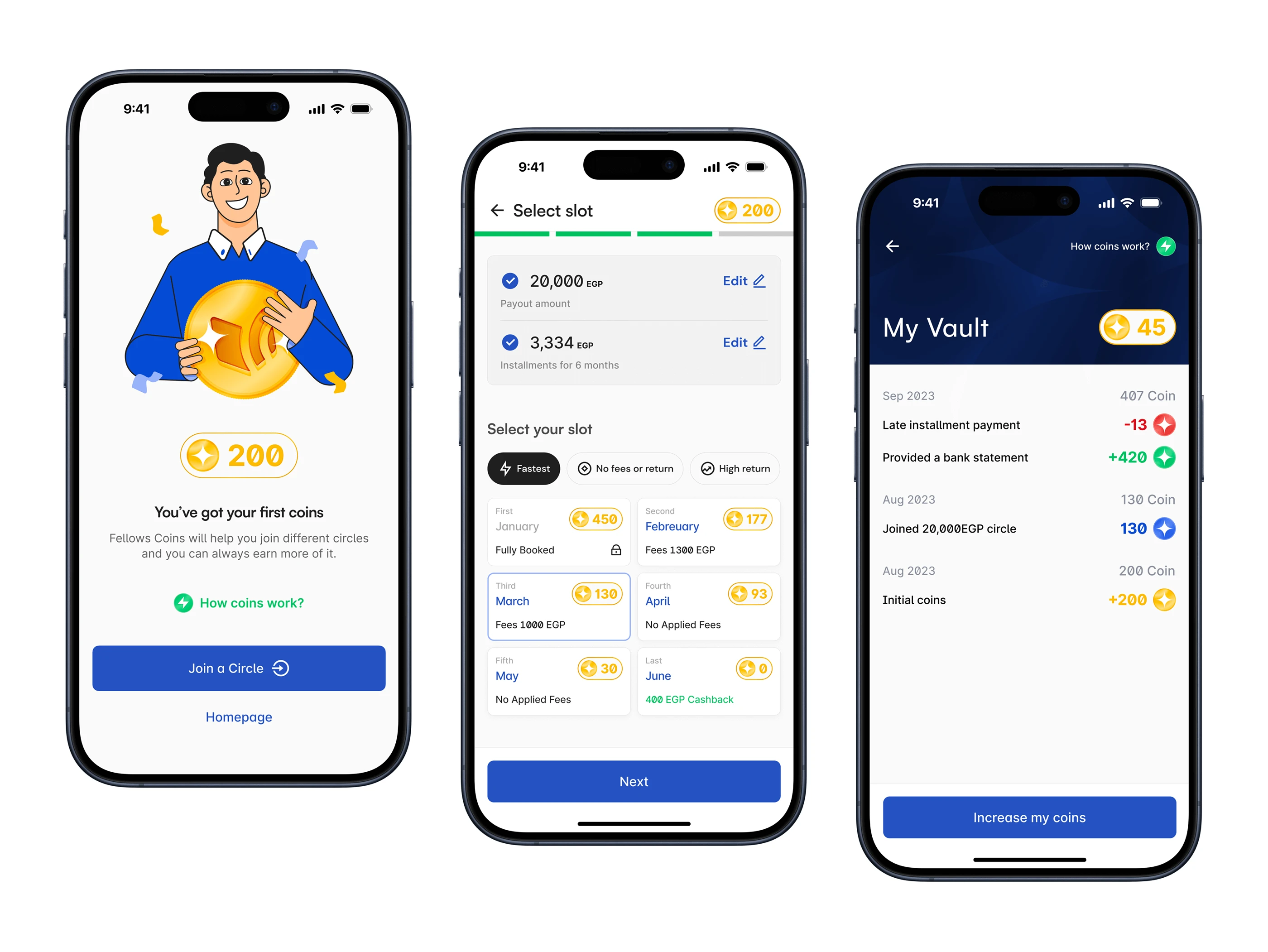

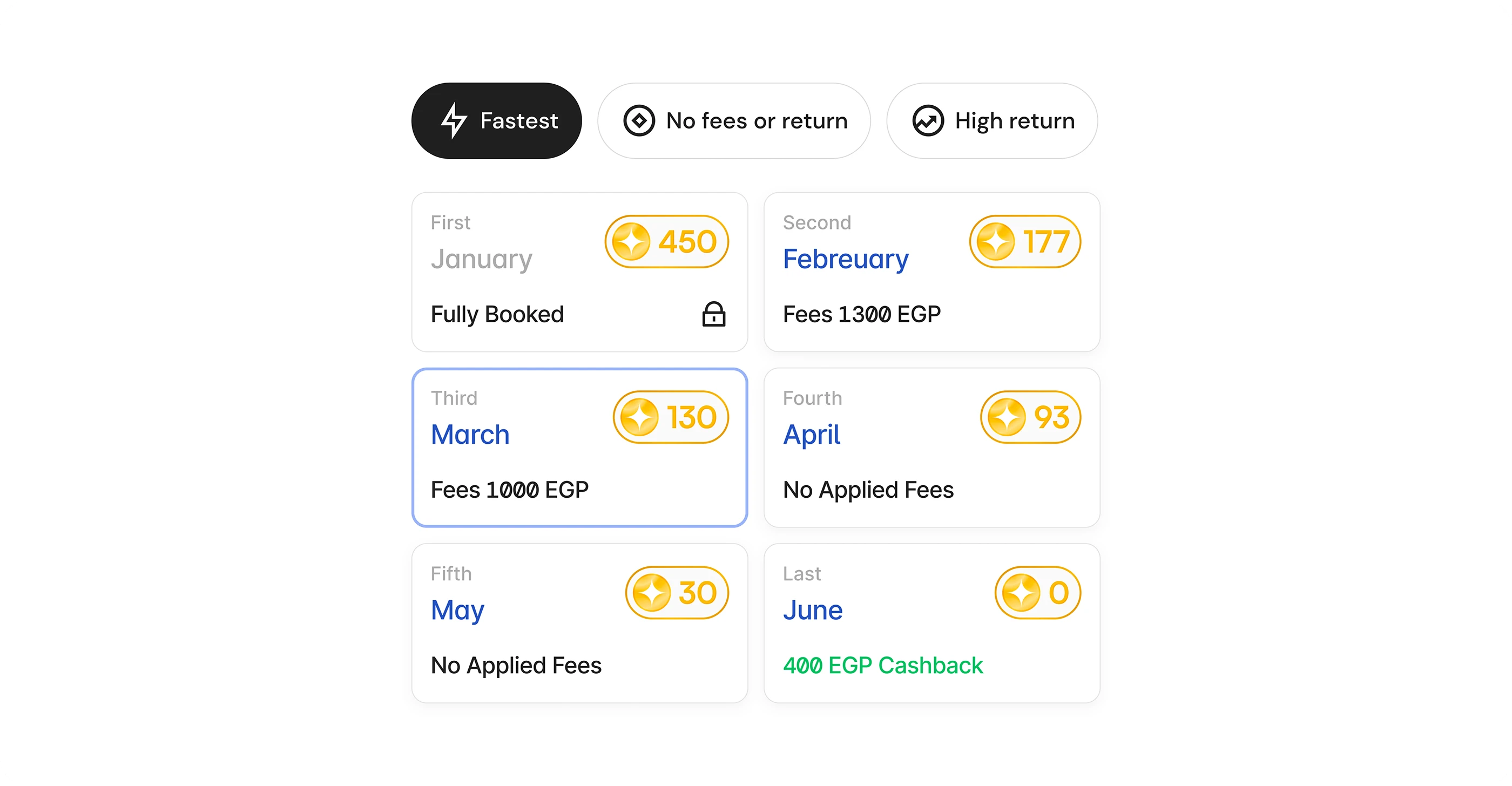

The design answer was gamification with real stakes. We turned creditworthiness into a coins mechanic: members build their limit through behavior the model can trust, and the interface makes the path to a higher limit legible instead of opaque. A risk model only works if the product around it collects honest signals and communicates decisions people can accept. I sat with the CEO and stakeholders throughout to keep the mechanic, the model, and the business case aligned.

How the teams worked

Cross-functional projects fail in the seams, so I spent deliberate effort on them. I facilitated workshops that mentored designers, aligned engineers around the Figma workflow and design system, and walked stakeholders through new experiences before they shipped. The same period included rebuilding the design system's usability — designer satisfaction rose by 60% — which made every downstream collaboration cheaper.

Outcomes

The credit assessment shipped with the ML model in production: default rates dropped by 12%, exposure decreased by 56M EGP, and retention lifted by 10%. It remains the clearest proof point in my work that design earns influence by moving the numbers the business actually runs on.